Silicon Valley Bank Crisis

What went wrong?

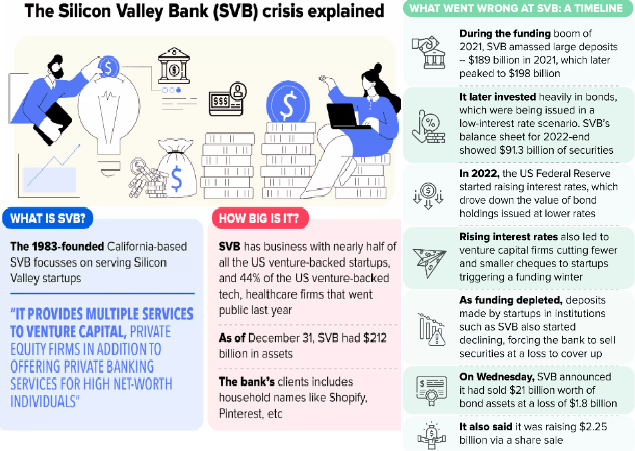

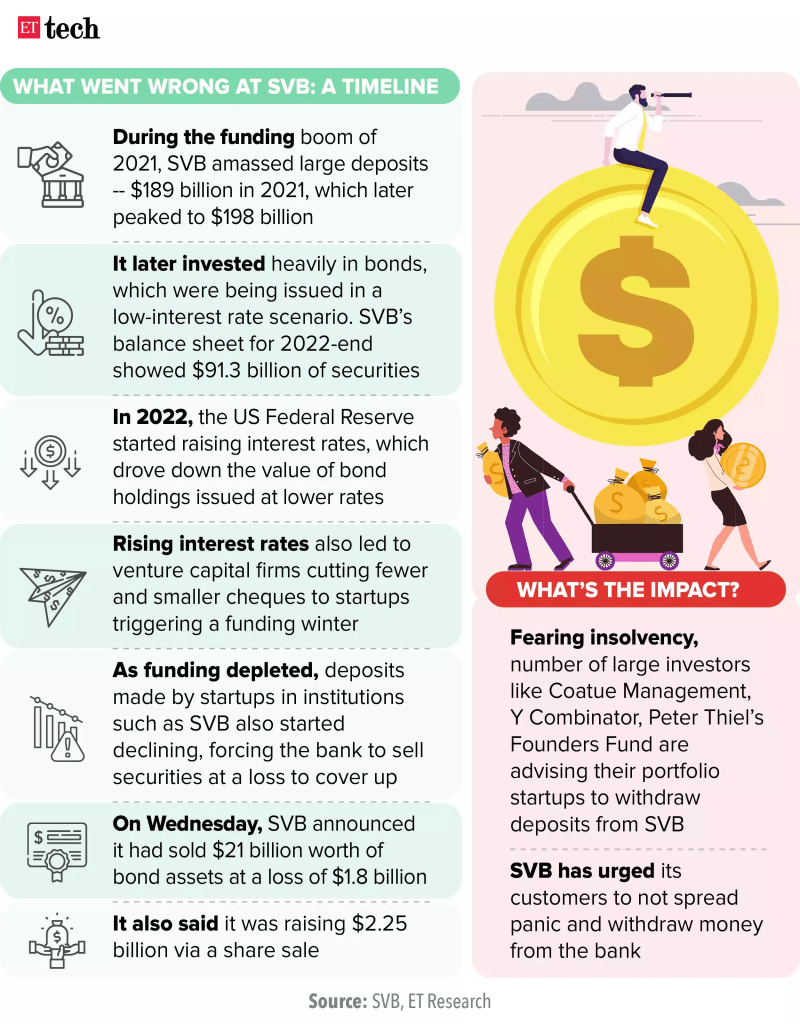

- During the funding boom of 2021 SVB amassed large deposits around 189 billion dollars which later peaked to a massive 198 billion dollars.

- SVB later invested heavily in bonds(mostly into mortgage bonds and treasuries) which were issued in a low interest rate scenario.

- The bank’s balance sheets for 2020 to end showed 91.3 billion dollars of securities but the problem started in 2022.

- SVB needed to acquire other interest-bearing assets.

- The federal reserve started raising interest rates which drove down the value of bond holdings issued at lower rates.

- Rising interest rates also led to venture capital firms cutting fewer and smaller checks to startups that triggered a funding winter as funding depleted.

- Venture capital funding was drying up, companies were not able to get additional rounds of funding for unprofitable businesses, and therefore had to tap their existing funds.

- Since banks make money on the spread between the interest rate they pay on deposits and the rate they are paid by borrowers, having a far larger deposit base than loan book is a problem.

- Deposits made by startups in institutions such as SBB also started declining. This in turn forced the bank to sell securities at a loss to cover up. The bank also said that it was raising 2.25 billion dollars via a sale of shares.

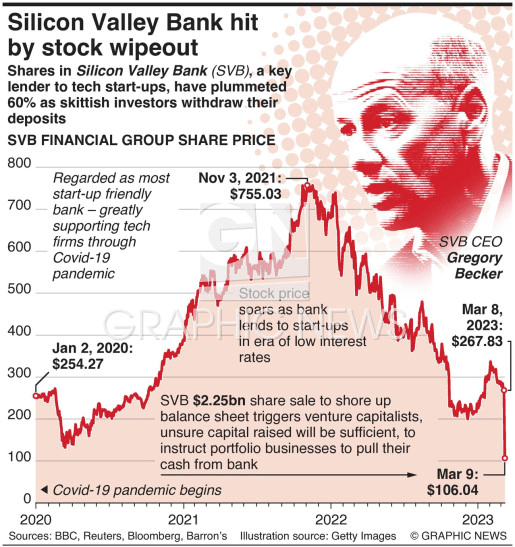

- SVB Chief Greg Becker sold 3.6 million dollars in stock days before the bank’s failure.

What is the impact?

- Fearing insolvency, a number of larger investors like the Y combinator, Peter Thiel’s Founders Fund are advising portfolio startups to withdraw their deposits from SVB.

- The US Bank index fell by 7.70%.

Impact on India

- The biggest impact of the collapse will be on Indian startups especially the ones funded by the American incubator the Y combinator.

- About 60% of YCombinator’s startups with Indian founders have exposure to SVB.

- Indian startups have to flip their corporate entities to the US to get the funds.

- But if the financial market in the west continues to decline and there is a recession it will affect the Indian financial markets and result in lower growth rates in India.

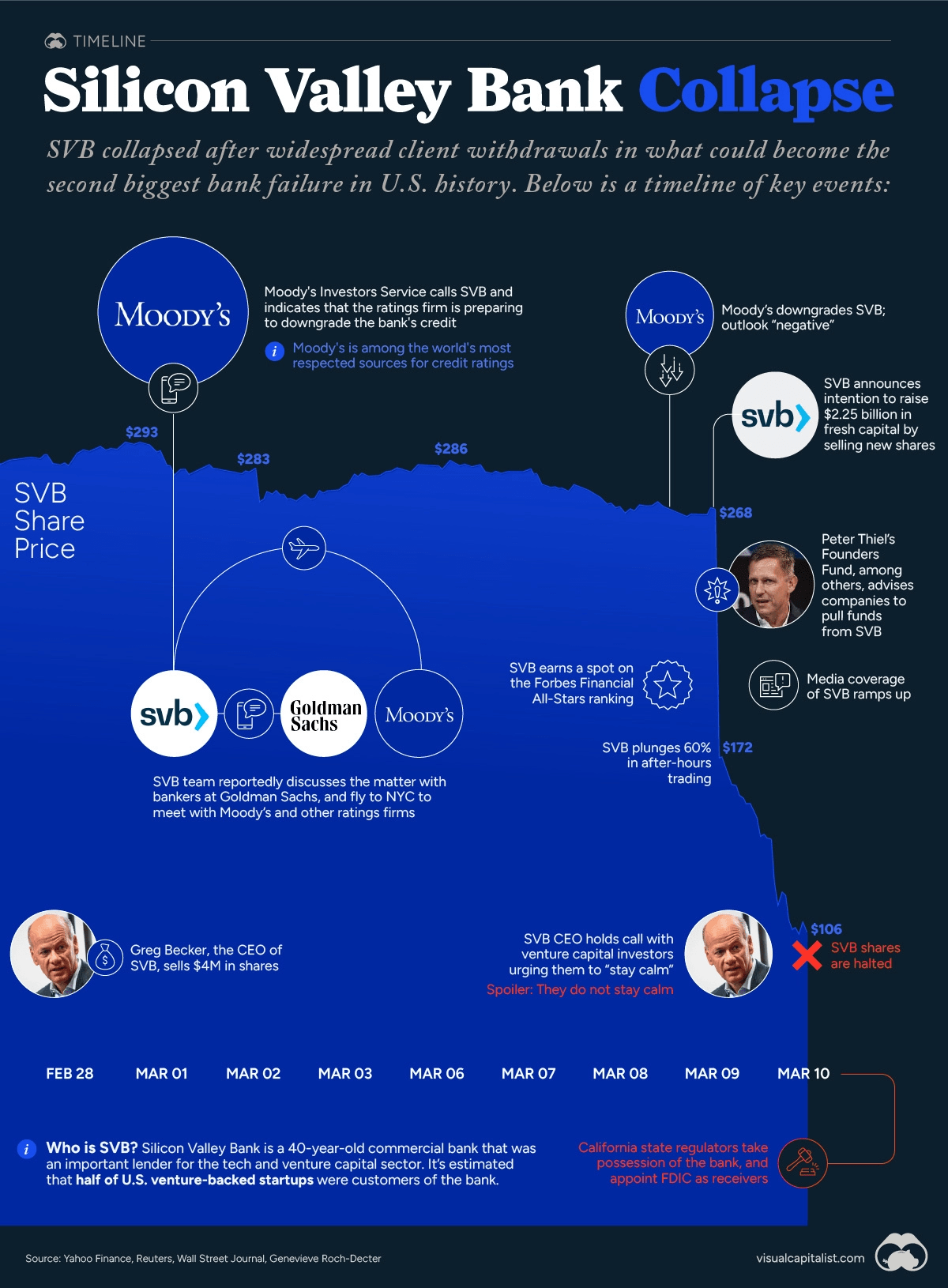

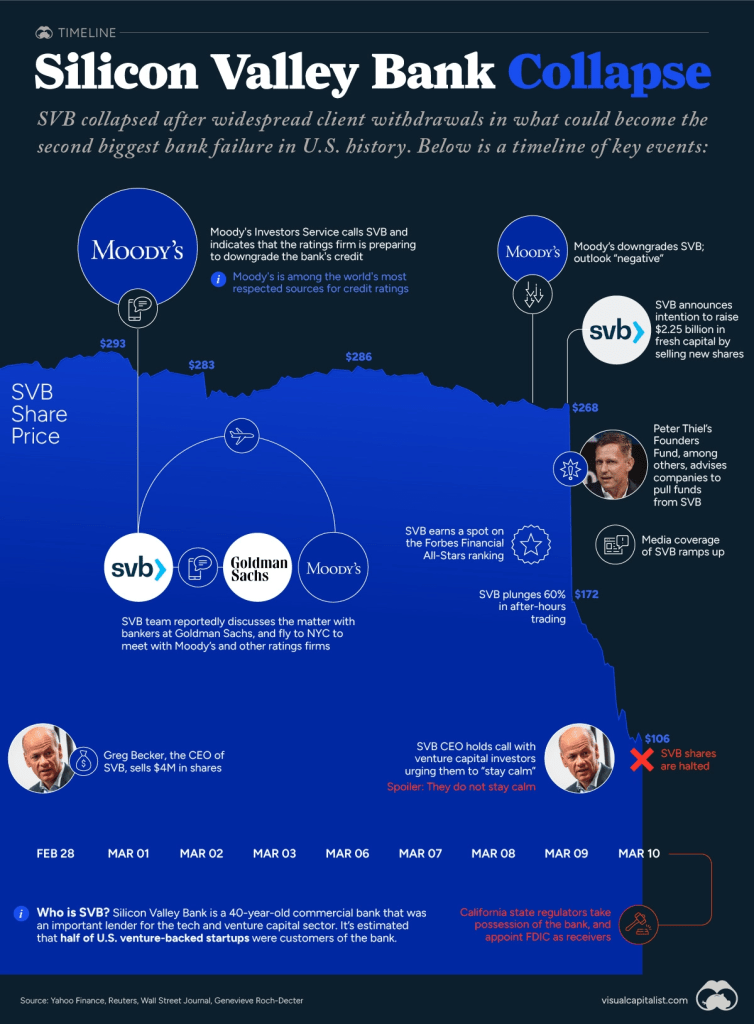

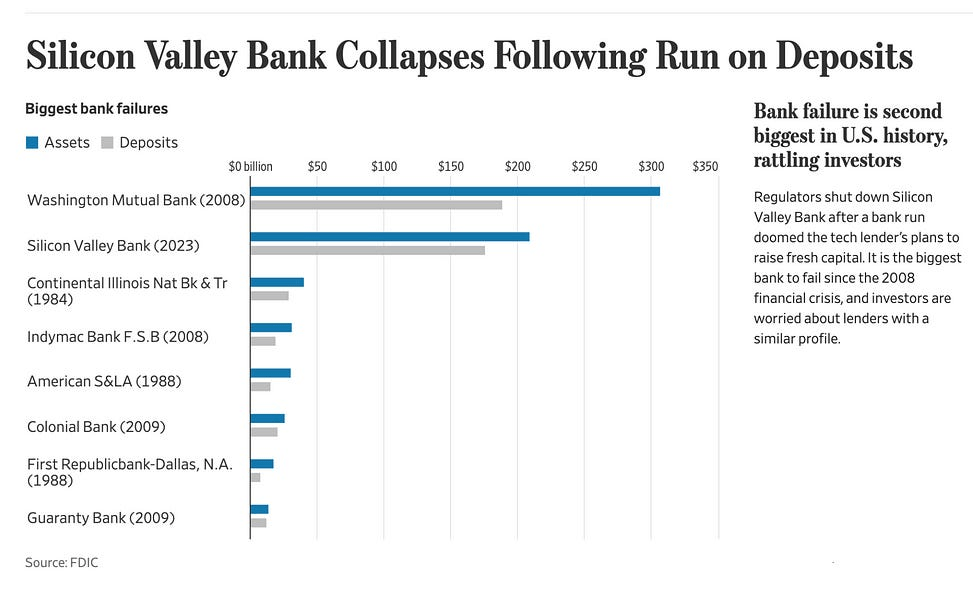

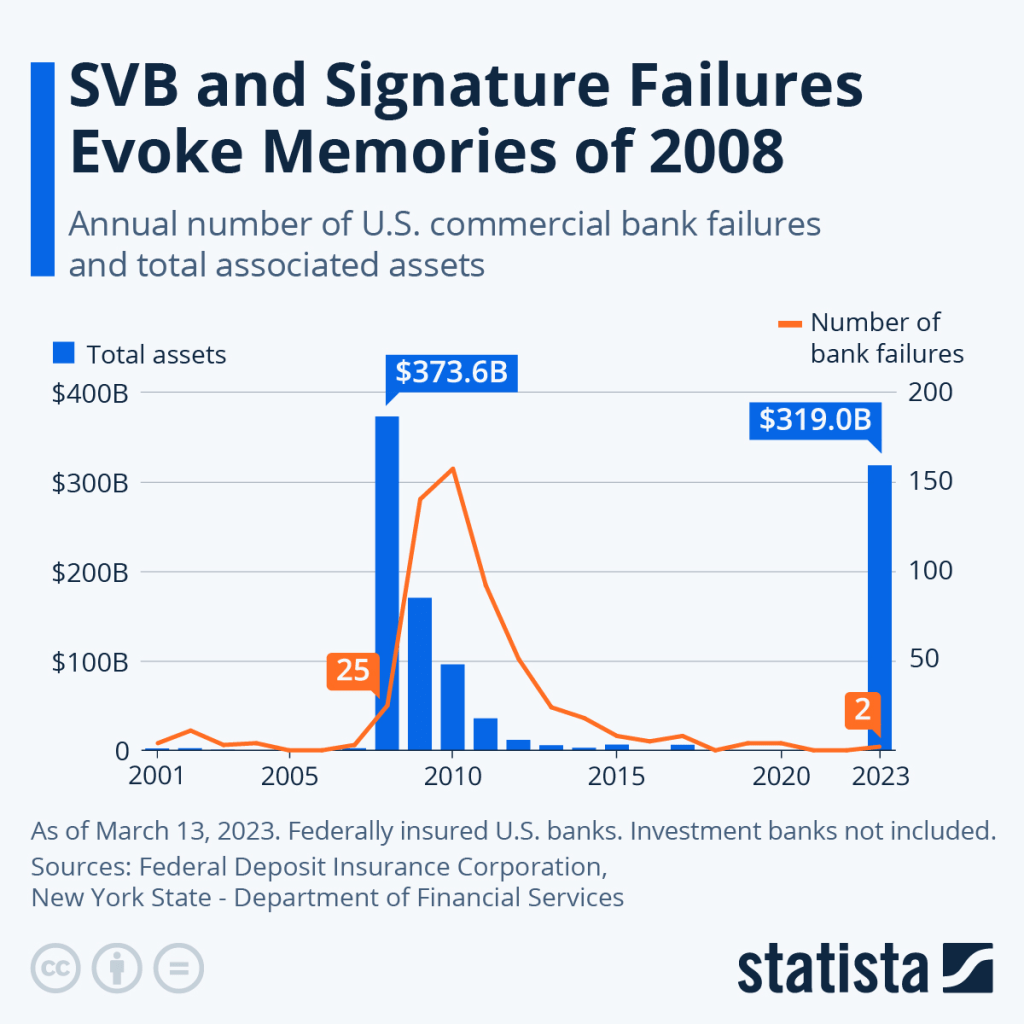

While the “biggest US bank failure since 2008” may sound like a foreshadowing of the crashes and contagion that shook Wall Street in the run-up to the Great Recession, this case is quite different. The general risk of knock-on effects has decreased as regulation has tightened. SVB was also more of a lender than an investor. Covid-time easy money had resulted in an increase in deposits held by SVB’s startup clients, a large portion of which was invested in bonds (think lazy banking) that plummeted in value as the US Fed abruptly reversed its monetary policy to combat inflation.

As a tech-sector squeeze resulted in withdrawals that forced bond losses and revealed a gap in need of capital infusion, a panic run on SVB ensued. Less lazy US banks are also vulnerable to bond portfolio damage, but it is less of a concern for them because their assets and liabilities are more diverse and thus less risky. There have been calls for SVB bailouts, but only if it poses a systemic risk would a federal rescue be justified. At this point, SVB’s failure has not reached such proportions, even if some startups suffer, and it’s best for the rest of us that it doesn’t.

WHAT HAPPENS NEXT?

- There are two large problems remaining with Silicon Valley Bank, but both could lead to further issues if not resolved quickly.

- The most immediate problem is Silicon Valley Bank’s large deposits.

- The Federal government insures deposits to $250,000, but anything above that level is considered uninsured.

- The Federal Deposit Insurance Corporation said insured deposits would be available on Monday morning.

- At the moment, all of that money can’t be accessed and likely will have to be released in an orderly process.

- But many businesses cannot wait weeks to get access to funds to meet payroll and office expenses. It could lead to furloughs or layoffs.

- There’s no buyer of Silicon Valley Bank.

Typically bank regulators look for a stronger bank to take on the assets of a failing bank, but in this case, another bank hasn’t stepped forward, buying Silicon Valley Bank could go a long way to resolving some of the problems tied with the money that startups can’t get to right now.

KUMAR-ARCHIT

STUDENT

INTERNATIONAL BUSINESS & FINANCE